Lenders know that the foreclosure process is an arduous process that lenders, especially small lenders, want to avoid if at all possible. Yet, when alternative resolution methods have been exhausted, lenders will enter the foreclosure process in order to protect their assets.

Many small-to-medium lenders may be foreclosing on a property for the first time, which might make the process look overwhelming. The foreclosure process varies from state-to-state. Additionally, compliance is crucial, and any missteps can result in crippling consequences for the borrower, including delays and lawsuits.

Commercial real estate foreclosures will always be either judicial or nonjudicial. Below is everything that lenders should know about the nonjudicial foreclosure process before enacting one. Because the foreclosure process is complicated, lenders should rely on third-party trustees to guide them through.

What is a Deed of Trust Versus a Mortgage?

Whether a property is foreclosed by a judicial foreclosure or a nonjudicial foreclosure is related to how the property is secured. Nationally, commercial real estate properties secured by a loan are either secured by a deed of trust or a mortgage. While the word “mortgage” is often used interchangeably to describe deeds of trust and mortgages, both are different.

Whether properties are secured through a deed of trust or a mortgage depends on the state. Judicial-only states secure property loans through mortgages. Mortgage agreements include two parties — the lender and borrower. In a mortgage agreement, the borrower holds onto deed with lien on the property. A mortgage must be foreclosed judicially

Nonjudicial states secure loans through deeds of trusts. A deed of trust agreement includes three parties — the lender, the borrower, and a third party trustee who holds the property deed. Deeds of trust will usually include a power of sale clause, giving the lender the power to foreclose and sell the property in the event of a default on behalf of the borrower.

States that are both judicial and nonjudicial can have commercial real estate properties secured by either mortgages or deeds of trust.

What is the Difference Between Judicial and Nonjudicial Foreclosures?

Commercial Real Estate Judicial Foreclosures

In a judicial foreclosure for commercial real estate, the lender must file a lawsuit with the court, triggering the borrower to receive a summons and a copy of the complaint. The borrower is given time to contest the complaint.

If the judge denies the contest, or if there is no contest, the property is auctioned by the court, oftentimes on the courthouse steps. If there is not a high enough bidder, the property is sold to the lender, and the lender becomes the property owner.

Commercial Real Estate Nonjudicial Foreclosures

In a nonjudicial foreclosure of commercial real estate, the lender is authorized to foreclose the property through the power of sale clause in the agreement. Lenders can then foreclose a property without the need to go through the court.

Typically, the borrower issues a notice of default, giving the borrower a chance to cure the default. After the waiting period, the lender will issue a notice of sale. The foreclosure process and the property sale is typically conducted by the third-party trustee.

Related Post: Nonjudicial Foreclosure Process: What Commercial Real Estate Attorneys Do

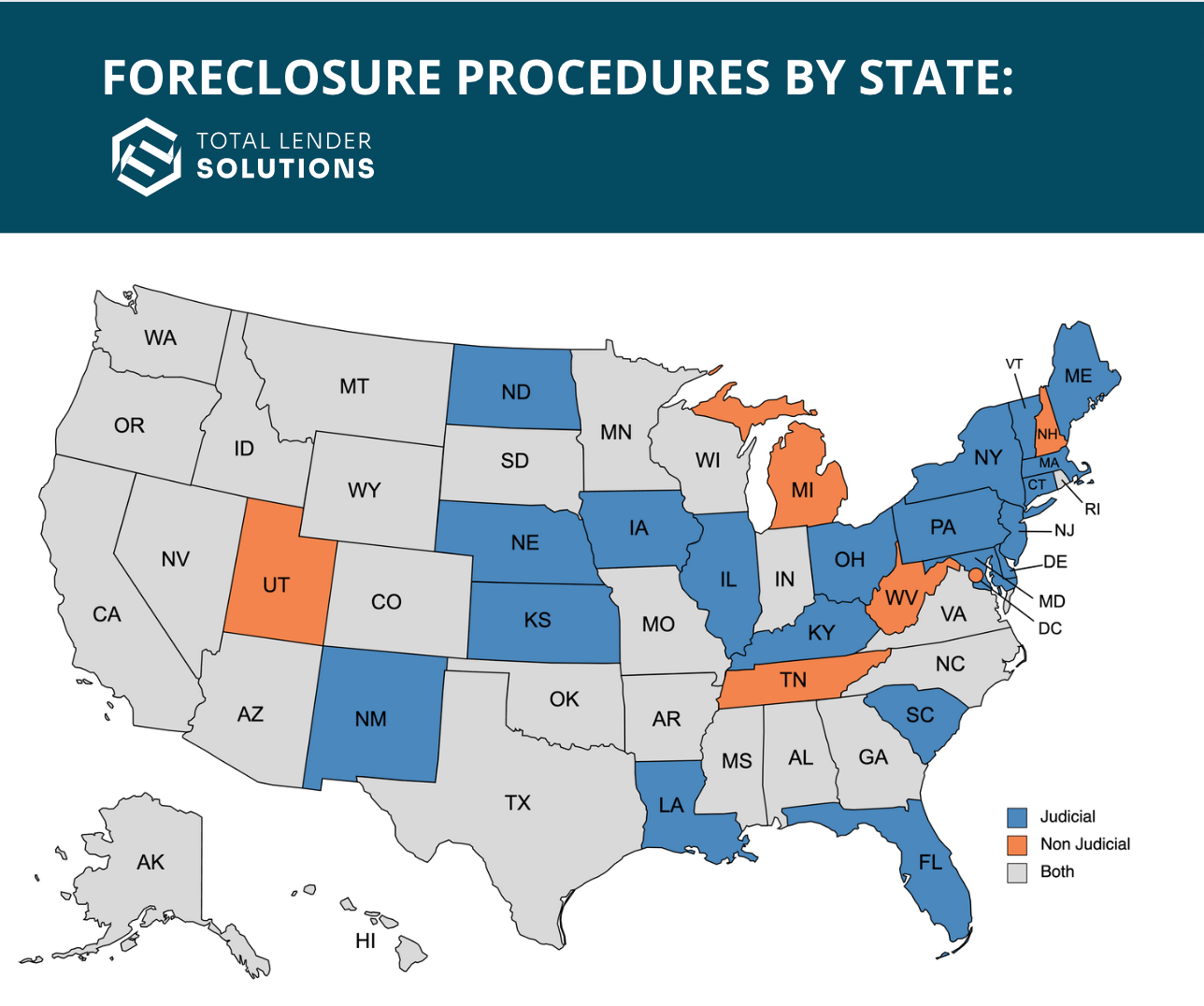

Foreclosure Procedures by State 2022

States with Judicial-Only Foreclosure Procedures

Connecticut, Delaware, Florida, Illinois, Indiana, Kansas, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Nebraska, New Jersey, New Mexico, New York, North Dakota, Ohio, Pennsylvania, South Carolina, and Vermont

States with Nonjudicial-Only Foreclosure Procedures

Michigan, New Hampshire, Tennessee, Washington D.C., and West Virginia

States with Both Judicial and Nonjudicial Foreclosure Procedures

Alabama, Alaska, Arizona, Arkansas, California, Colorado, Georgia, Hawaii, Idaho, Iowa, Minnesota, Mississippi, Missouri, Montana, Nevada, North Caroline, Oklahoma, Oregon, Rhode Island, South Dakota, Texas, Virginia, Washington, Wisconsin, and Wyoming.

How to Nonjudicially Foreclose a Commercial Property

The timeline of a nonjudicial foreclosure varies state-by-state, but a nonjudicial foreclosure will usually happen in some variation of these stages: default, the notice of default stage, the notice of sale stage and the trustee sale. Depending on the state, there may be a redemption stage.

Default or Pre-Foreclosure

Once a borrower misses a payment, the borrower is in default. The time period between the initial default and the beginning of the foreclosure process is preforeclosure. A borrower typically has time in preforeclosure to cure the default before the foreclosure process is started. Typically, there is a waiting period before a lender can issue a notice of sale.

Notice of Default

A notice of default triggers the foreclosure process. Each state has requirements about how the notice of default must be delivered, published, or how often it must be delivered. A notice of default will usually include important details about the default and how to cure it. Some states may forgo this stage altogether, replacing it with a notice to cure stage or something of the type to alert borrowers that they are in foreclosure.

Notice of Sale

After a waiting period, lenders will issue a notice of sale. Each state has unique requirements about when, where, how often and to whom this notice should be published and what information should be included. The notice of sale will typically set up a sale date that must be set after a required waiting period, giving the borrower a chance to cure or contest.

Trustee or UCC Sale

Foreclosed properties are typically sold in a trustee or UCC sale. These sales are public or private on a date and time set by the notice of sale. Many states will not allow you to reschedule or postpone without following strict guidelines. In nonjudicial foreclosures, the sale is usually handled by the third-party trustee. If the bid is not met, the property is sold back to the lender.

Redemption Period

Some states allow a redemption period after the sale of the property, in which the borrower can buy-back or redeem the property.

Can I Get a Deficiency Judgment?

When foreclosing a property nonjudicially, there all typically be a deficiency that is not covered by the sale. Lenders are less likely to be able to pursue borrowers for this deficiency in nonjudicial foreclosures than in judicial foreclosures, but deficiency judgements are still possible in some states for nonjudicial foreclosures.

Commercial Real Estate Nonjudicial Foreclosure Timeline

How Long Does it Take to Foreclose a Commercial Property Nonjudicially?

The nonjudicial foreclosure process can vary widely depending on the state and on any delays that might arise. The nonjudicial foreclosure process can take anywhere from a few months to several years.

Common Delays in the Nonjudicial Foreclosure Process

Bankruptcy

If the borrower files for bankruptcy, all foreclosure activities must cease. The only action the trustee may be able to take is to postpone the sale date from time to time.

Temporary Restraining Order (TRO) Has Been Filed

A judge may sometimes issue a temporary restraining order on a lender running afoul. This ceases the foreclosure process until the restraining period is over or the ruling is overturned.

Active Litigation on the Property

If the borrower and lender is still seeking alternative resolution for the property, this may delay the foreclosure process so that litigation can continue.

Incomplete or Incorrect Intake Documents

Certain documents that need to be filed in order to complete a foreclosure include but are not limited to, the Substitution of Trustee, the Declaration of Compliance, and the Declaration of Default. Improper execution of these documents could delay the foreclosure process.

Missing Bidding Instructions

The lender must provide bidding instructions for the property sale. If the instructions are not filed in time, the sale can be postponed to a later date.

Nonjudicial Foreclosure by State

Arizona

In Arizona, once a loan goes into default, the foreclosure starts with the preparation and recording of a statement of breach. A notice of trustee’s sale is filed with the county recorder and includes the date, time, and location of the foreclosure sale.

The sale date must be at least 91 days after the notice of sale’s recording date. The notice of sale is sent by certified mail to the borrower within 5 days after the recording date. The borrower may either pay the loan off or reinstate the loan until 5 PM on the last business day before the date of sale. If the borrower fails to do so, the property can be sold at auction to the highest bidder.

California

In California, once a loan goes into default, foreclosure starts with the preparation and recording of a notice of default. From there, the borrower has three months to bring the loan current or pay off the debt.

If no action has been taken, the trustee prepares a notice of trustee’s sale. The notice is recorded, sent to everyone who was entitled to a copy, published once a week for three consecutive weeks in a newspaper, and posted on both the property and in a public place.

The borrower then has up until five business days before the sale date to cure the loan or up until the time of sale to pay the loan off. If the borrower fails to do either, the property can be sold at auction to the highest bidder.

Missouri

In Missouri, lenders send a breach letter to borrowers in default. Borrowers must be delinquent for 120 days before a notice of sale can be issued, and the sale is to occur 40 to 50 days after the notice.

Lenders must publish the foreclosure in a newspaper in the county where the property is located. Depending on the size of the town, they must publish either twenty times through to the day of sale, or once a week for four successive weeks, with the last one taking place the week of the sale.

Missouri Foreclosure Pricing Calculator

Nevada

In Nevada, if a borrower defaults, the lender must wait at least 30 days before issuing a statement that details the actions needed to cure the loan before the foreclosure process formally begins. If a property is owner-occupied, the law requires that the borrower have the option to participate in mediation. Thirty days after that, the trustee may issue a Notice of Default and Election to Sell. The borrower then has three months to cure the default.

Nevada requires that a separate “danger notice” be issued to the borrower. Once the three-month NOD mark has passed, the sale can proceed. The borrower must receive notice 20 days before the sale. The notice must be displayed in a public place, and published in a county newspaper once a week for the three consecutive weeks leading up to the sale.

Oregon

In Oregon, the borrower must be delinquent for 120 days before issuing a notice of default. For residential trust deeds, the beneficiary must offer mediation to the borrower. The notice of default and notice of sale are issued and recorded in the courthouse of the county where the property is located. The sale date is scheduled about 145 days out.

The lender must issue a danger notice to those holding residential trust deeds. The notice of sale must be published in a county newspaper once a week for four consecutive weeks leading up to the sale, with the last one being at least twenty days before the sale.

Texas

In Texas, once a loan goes into default the trustee sends the borrower a notice of default and intent to foreclose. This notice must be given no sooner than 20 days before the loan is accelerated. Once the loan has been accelerated, the trustee prepares and files a notice of trustee’s sale.

The notice of trustee’s sale indicates the date, time, and location of the foreclosure sale. The notice of sale is posted at the county courthouse and sent by certified mail to the borrower at least 21 days before the sale date. The borrower has three weeks before the sale date to pay the loan. If the borrower fails to do so, the property can be sold at auction to the highest bidder.

In Texas, all nonjudicial foreclosure auctions are held on the first Tuesday of every month.

Why Do Lenders Need a Foreclosure Service?

1. Navigate the Complex Nonjudicial Foreclosure Process

For small to medium lenders encountering their first foreclosure, the process can be overwhelming and daunting. A foreclosure service provides answers and comes up with solutions for uniquely complex problems. Lending teams are never left in the dark about the status of their foreclosure.

2. Compliance

Lenders are subject to many compliance codes depending on their state, from statewide homeowners’ bill of rights, to federal laws like the Fair Debt Collections Practices ACT (FDCPA). Failure to comply with code can result in serious consequences for small lenders, including lawsuits and financially devastating delays. Foreclosure services are well-versed in foreclosure compliance law and can ensure that lenders stay above board.

3. Streamline the Process

Lenders often do not have the time to handle the foreclosure process. When lenders bring on a foreclosure service, the service can work hand-in-hand with the lender, freeing lending teams to focus on their customers instead.

The Premiere Nonjudicial Foreclosure Company for Your Commercial Real Estate Foreclosure Services

At Total Lender Solutions, we advocate for lenders looking to maximize recoveries on defaulted loans in Arizona, California, Missouri, Nevada, Oregon, and Texas. For over 15 years, our team of highly experienced real estate professionals and legal experts has transformed complicated processes into clear resolutions for institutional and private lenders. We work as a vigorous extension of your team to provide comprehensive solutions and seamless communication, from pre-foreclosure and notice of default to the final sale phase. Our dedication and persistence when it comes to the foreclosure process ensures that our clients feel confident in reaching a successful outcome. Contact us today.